Why do I need to make an export declaration?

Since 2009, customs only recognizes export declarations that are submitted in digital form. This made all the paperwork obsolete in one fell swoop and left people faced with the problem of now declaring their exports online.

An online export declaration seems quite simple at first glance, but when confronted with the issue, questions quickly arise:

- When do I have to register my goods?

- What information do I need for my declaration?

- And above all: How does an export declaration work?

To make your question marks disappear, we at BEX Components AG have summarized and explained the 8 most important steps of an export declaration in the two-step simplified procedure for you.

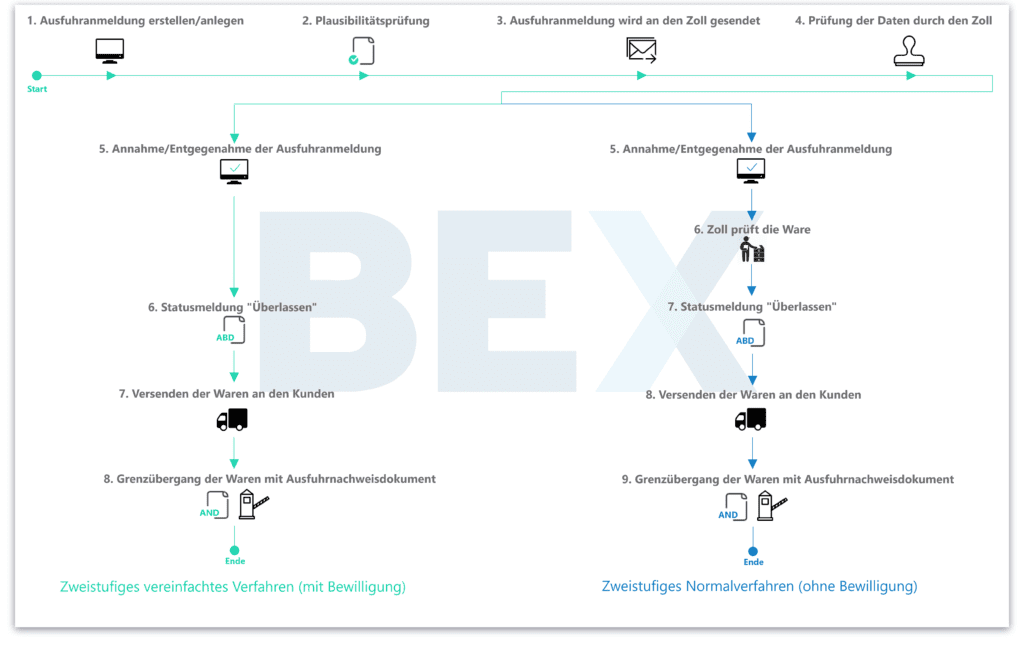

1. Create an export declaration

Shipments of goods to other EU countries usually have to be declared to customs if the value of the goods exceeds € 1,000. In some cases, however, a declaration must also be made for smaller amounts, such as for dual-use goods.

You have two options to declare your goods:

a) Manually via the IAA PLUS portal from customs or another export solution

For this you need the invoice and the delivery bill of your shipment. These documents usually contain all relevant data for your declaration.

b) About the integration of an export solution into your ERP system

In this process, a large part of the declaration data is automatically transferred from your ERP system to the export declaration.

2. Check the data

Before an export declaration is finally sent to customs, all the data entered is cross-checked using an error check specified by customs. This plausibility check primarily queries whether the formats, field lengths and field dependencies specified for a declaration are adhered to.

3. Send the export declaration to customs

If your export declaration has successfully passed the plausibility check, your data will be transmitted to customs, this can be done in two ways:

a) Independently via portal

Here you send your registration data directly via the IAA PLUS portal from customs

b) Via an export solution

Either you transmit your data directly to customs

or

Your data is sent to customs via the export solution provider as a decentralized communication partner.

4. Have the information verified by customs

Once the data has been received by customs, it is checked again for plausibility. Here, the focus is primarily on the correctness of the content, such as whether all goods are included in the specified authorization.

5. The acceptance of the declaration by the customs

If no error is found even during the second check by customs, customs accepts the order. Each operation accepted by customs is assigned an individual MRN by which it can be identified.

If there is an authorization on your part, your declaration goes directly to the status of release. This is called declaration in the two-step simplified procedure (green route).

If there is no authorization, customs must first examine the goods before releasing the transaction. The declaration is therefore carried out in the two-stage normal procedure (blue route).

6. The transfer of the application and the ABD

After your goods have been successfully declared and accepted or inspected by customs, your transaction is given the status of release by customs. You will receive the Export Accompanying Document (ABD), which replaces the export declaration in paper form and must accompany each of your consignments of goods.

7. Send the goods

Once you have received the ABD, you can ship your goods together with the export accompanying document and any accompanying documents. The three most commonly used documents are the ATR, the IP and the EUR1.

8. The goods cross the border and leave the EU

When the goods leave the EU, they are checked and recorded at the last customs office. A proof of export document (AND) is issued, which proves that the goods have left the country legally.

What to do if the goods have left the EU but you have not received a proof of export document? In this case, customs has not recorded your shipment. It is now up to you to prove through documents and receipts that your goods have left the EU and arrived at their destination. This process of resubmission is also called tracking.

Now you know the most important points of the export declaration and have hopefully gained a deeper insight into some customs terms. If some terms are still unclear to you, feel free to have a look at our glossary/FAQ!

Do you want further support with your export declarations? Then our export solution AES3 is just right for you.

Glossary ATLAS Export Declaration – FAQ

What is a customs office of export?

The customs office of export is the competent customs office of the place where your goods are dispatched.

What is a customs office of exit?

The customs office of exit is the customs office where your goods cross the EU border. It is often difficult to know exactly where your goods will leave the EU. Therefore, in some cases, it is sufficient to indicate the designated customs office of exit.

What does MRN mean?

The Movement Reference Number (MRN) is a unique registration number assigned by customs. It is the most important reference for the customs declaration and is used by customs to allocate and process your transaction and to identify the associated consignments.

Export Accompanying Document (ABD)

The Export Accompanying Document (ABD) is a proof document about the admissibility of your export. It must always accompany the associated consignment of goods, as it contains the MRN and a barcode and thus replaces the export declaration in paper form for the inspecting customs office.

Export verification document (AND)

You will receive the export document after your shipment has passed the customs office of exit. It is the confirmation from customs that the goods have been checked and have left the border legally.

If your goods have left the border and have not been registered by customs, you must prove that the goods have crossed the border by resubmission (tracking) to customs with your own documents.

What is the difference between main pack and side pack?

A by-pack is a good that is included in the packaging of another item of goods. Both items must be declared in the same export declaration.

What do the abbreviations CO, EFTA & EX mean?

CO goods are common goods which

- have been manufactured within the EU and have not been supplemented with parts from third countries

- or supplemented or built with parts from a third country, but which is allowed to trade duty free with the EU.

EFTA goods are goods traded within the countries belonging to the European Free Trade Association (EFTA).

EX goods are goods that are sent to a third country without a free trade agreement. Here, customs duties are incurred for the transfer.

What are Incoterms?

Incoterms are guidelines that are adjusted annually. These voluntary rules relate to your contract and your delivery and can be included in the commercial contract with the agreement of your trading partner. You can see which Incoterms exist and which will apply from 2020 here.

The exporting country or the country of destination

The country of export of your shipment is the country where your goods originate and from where they are shipped.

The destination country is the country where you want to send your goods. Importantly, the country of destination is the last country your goods will arrive in, any countries passed in between are only relevant to your transport route.

Means of transport

The means of transport at the border indicates the transport vehicle with which your goods cross the EU border. This could be, for example, by air freight or sea freight.

What is the difference between the gross mass, net mass and total mass?

In order to correctly declare your shipment of goods, you must submit all relevant dimensions of your shipment to customs.

These are:

- the gross mass of your individual goods items, i.e. the weight of your goods plus the weight of their packaging

- the net mass of your goods, i.e. the actual weight of your respective goods items without their packaging

- the total mass, which is the total weight of all goods items of your shipment with their packaging in total

Accompanying documents and movement certificate

Accompanying documents are documents that accompany your goods on their way to the end customer.

The most important of these are:

- Waybill

- Delivery bill

- Loading slip

Movement certificates are documents that certify your goods, depending on their origin, as duty-free or subject to lower customs duties.

The most commonly used are:

- EUR1: This certificate is considered as preferential proof, it is attached to goods traded within bilateral and multilateral agreement countries of the EU. It is recognized as a certificate of origin in the foreign trade sense.

- ATR: You enclose this certificate with goods that you trade directly between an EU member state and Turkey in the free movement of goods.

- IP: The abbreviation IP stands for certificate of origin, so the IP is a document that certifies the actual origin of your goods.